Peloton (Part 3): Business Model, Challenges and Opportunities

Episode 20: The third and final part in a series on Peloton Interactive

This is Part 3 of the 3 part series on Peloton. Hopefully you made it through all three!

Part 1: In the first part of this series on Peloton I covered it’s products, content, community and the competitive landscape for at-home fitness.

Part 2: Focuses on how Peloton beefs up its supply chain to reduce delays, and then how Peloton will subsequently attract new customers once demand dies down. It covers three pieces: Supply Chain, Marketing, Market Size (new geos, products, and channels).

Part 3: This final part finishes with Peloton’s business model as well as upcoming challenges & opportunities.

Business Model

Peloton’s core business of acquiring and retaining connected fitness user is money printing machine.

Acquiring Connected Fitness Users

Take a look at some numbers Nikhil Joshi pulled from Peloton’s investor documents:

During fiscal 2020:

Peloton sold $1.5B worth of Connected Fitness Products.

They added ~580,000 Connected Fitness Subscriptions.

These subscribers spent on average ~$2,600 ($1.5B / 580k) to buy the Connected Fitness Product (connected fitness product is required to activate the subscription).

At 43% gross margin for the Connected Fitness Product, gross profit was at ~$1,150 per product ($2,600 * 43%).

The cost of acquiring this customer was ~$800.

This means that Peloton makes ~$250 (1,150-800) on the hardware purchase alone! (On top of the subsequent subscription revenue!)

High performing SaaS companies have an average Customer Acquisition Cost (CAC) payback period of 5-7 months. This means it takes them ~6 months of subscription revenue to recover the marketing and sales costs of getting the customer.

Peloton’s CAC payback period is less than one month. (Maybe even less since they get paid when the customer purchases, but with delays aren’t shipping the product for a few months.)

Retaining Connected Fitness Users

On top of their solid acquisition numbers, Peloton has averaged a 0.64% net monthly customer churn since 2017. Which means in last 3 years >80% of connected fitness subscribers are still with Peloton.

Peloton has used product innovation to cement subscribers even further. If you subscribed in 2017 you have to be happy with the value you've gotten through the years with the addition of all the new instructors and class types.

In next three years they could turn $40/month price into a steal by continuing to add value to the subscription.

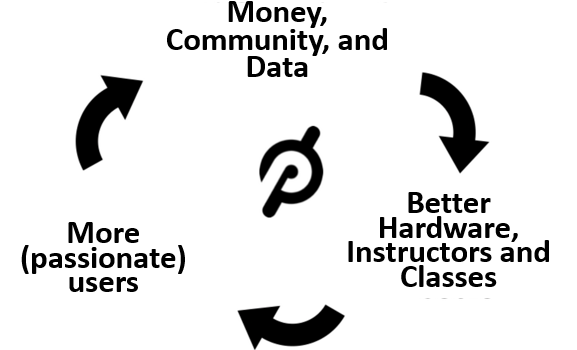

This is Peloton's cash cow. The connected hardware requires a large upfront investment, which is both profitable and locks in customers to a subscription.

As long as Peloton keeps improving its hardware, instructors and class experience, it will attract more users and the resources (money/community/data) to invest back into the products.

Business flywheels are becoming a little cliche, it’s a helpful way to think about a buisness.

Challenges & Opportunities

Even given Peloton’s insanely profitable model, it has a number of challenges to meet it’s crazy goal of 100 million subscribers and continue growing. (It has 3.1 million subscribers now and it’s stock is up 6x this year)

The goal of this final section to dive more deeply into some of Peloton’s challenges and opportunities I covered in the previous two parts.

Challenge #1: Omni-channel

As I said in part 1, “it's generally assumed that post-covid: work will be hybrid office/home, commerce will be omni-channel, and healthcare will be a hybrid tele/office model. My guess is that fitness follows that path.”

Opportunity: Peloton has the opportunity to be the gym-agnostic provider of equipment.

The Precor acquisition makes it clear that Peloton likely doesn’t want to follow the path of Equinox/Soulcycle and build out a bunch of studio locations. It wants Pelotons in YMCAs, hospitals, apartments and even your office.

This is a win-win for Peloton and those locations. Especially for struggling gyms and apartment complexes having a Peloton will attract new customers.

It may cannibalize existing Precor equipment already in those locations, but the Peloton omni-channel ecosystem will be so much stronger. Users will be able to workout at home, in the gym or at the office and sync seamlessly.

Challenge #2: Diversify its product lineup

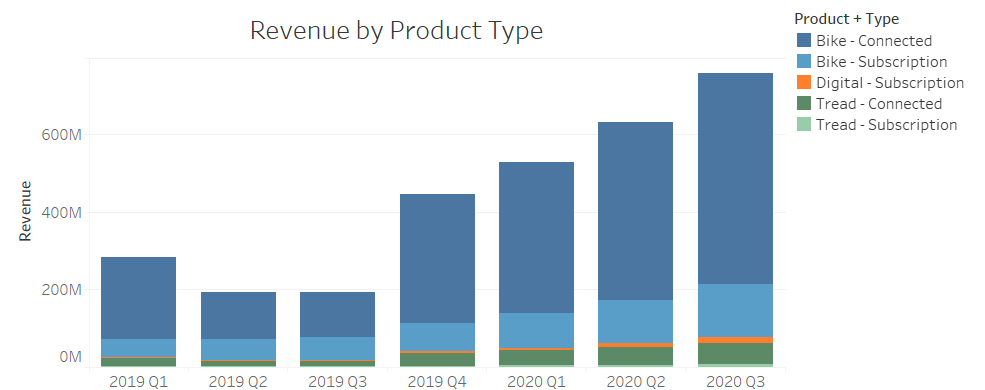

Peloton is a one-product company in terms of revenue and profit generation.

More and higher reviews for the Bike (though has been around for a couple more years though)

Peloton does not break it out, but The Flywheel estimated Peloton’s reliance on the Bike by product using the ratio of Bike to Tread reviews and workout ratings. (ex. Bike rides on average had 4-5,000 ratings within 2 or 3 days. Tread runs had fewer than 200.)

Using those numbers we can say conservatively that connected Bike users likely make up 95% of connected users. Given that ratio, I estimated sales and profit by product and type of purchase:

*These are all estimates using the fact that 95% of connected sales are likely Bikes.

In Q3 2020 Peloton likely got as much as 90% of its revenue from Bike subscribers (hardware and subscription).

Opportunity: Can it find another hit like the bike?

This is another perhaps bigger reason for the Precor purchase. Peloton realized that they are heavily reliant on Bike sales, so if the market gets saturated they want the ability to expand to other products.

Precor gives them the ability to diversify, and hope one of these can become as big of a hit as the bike.

Peloton can create or latch on to the next workout fad with this ability to manufacture many different types of equipment.

The next workout fad… Elliptical Dance

Challenge #3: Data Integration

Peloton tracks decent data for each ride, run or workout, but can track more to improve user experience.

Class: class type, instructor, difficulty, rating, and % completion

Bike: cadence, resistance, distance and output

Tread: speed, elevation, distance, and output

Digital: calories burned

Opportunity: Build more integrations and share metrics to improve performance.

The above metrics help you understand what you did, but don’t help you perform better.

For example, right now you can connect Peloton to Apple Watch, Fitbit and Strava but you cannot directly track your heart rate on the Peloton bike using these devices. If Peloton improved the tracking to include metrics like heart rate and steps it could personalize workout recommendations.

Additionally purchasing a watch company like Whoop would give it so much more data to help improve performance. (Whoop has the perfect hardware + subscription DNA to fit with Peloton.)

Challenge #4: Marketing

In Part 2 I showed this image of the similarity of Peloton vs Echelon Fit ads.

Peloton can’t afford to market itslef just like any other brand.

Opportunity: Unique marketing that stands out and takes advantages of Peloton’s strengths with data.

Peloton does a good job of using workout history to celebrate achievements with markers like badges and the Century Club (once you reach 100 rides you get a shout out in a live class, a free badge and t-shirt). But people love sharing and they could do even more!

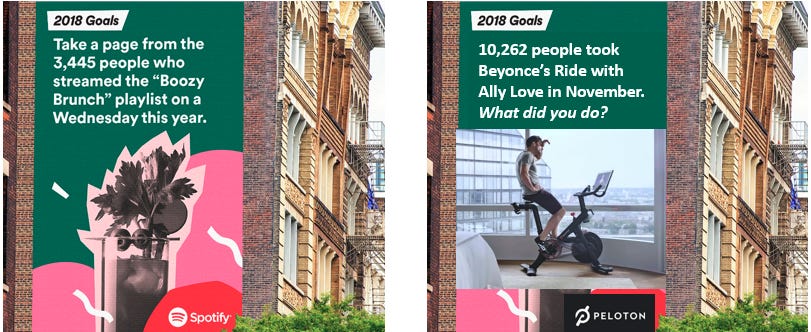

Spotify has two good examples of how to take advantage of data in marketing:

What about using more of the data to create a Spotify Wrapped-esque summary? (Peloton does a version of this, but it can become much more powerful as they track more data and get more users)

What about a marketing campaign showing stats in your areas?

Maybe I shouldn’t be a copywriter…

Conclusion: Prove Peloton isn’t a workout fad.

Crossfit, P90X, Bowflex, TRX bands, Shake-weight

Every single one of these actually works quite effectively. This is the big secret of the exercise industry. The type of workout does not matter if you don’t do it regularly.

In addition, churn is the default option. It’s very easy to stop working out. And due to low switching costs it’s also very easy to ditch Peloton and go back to gym, use YouTube, or even pick up the next fad.

Peloton is new and exciting, so it has replaced Crossfit, P90X, etc. as the current fad.

How can it continue to be new and exciting? Continue to focus on and improve the user experience.

This means continuing to:

build its community through features like two-way video

offer more classes and class types

utilize the power of its internal celebrities (instructors) and external celebrities (Beyonce/Tiesto group rides)

offer an omni-channel experience in homes/gyms/offices

In competing with all-encompassing tech giants like Apple, boutiques like SoulCycle and box gyms like 24 Hour Fitness, Peloton must be focused on the user.

As shown in the above slide from CEO John Foley, it’s clear Peloton is willing to lose money and forgo profits to invest in product, experience, and expansion.

The (hopeful) end of the quarantine in 2021 will be a big test for the long term viability of Peloton.